Are There Food Delivery Wars Outside China? A UK Roujiamo Owner’s Answer

This is my seventh year living in the UK. Six years ago, I opened a roujiamo shop called Rogamo in a small town near Exeter. These days, the name has almost become the standard English term for roujiamo.

Before Rogamo, I had already spent ten years in the restaurant industry in China. When I opened my first shop in Beijing, group-buying—the precursor to food delivery—was just taking off. It was the era of the group-buying war. Street canvassers came to the shop every day, urging us to join group-buying and using various subsidies to entice both consumers and merchants. Looking back, the group-buying war was precisely the precursor to the delivery subsidy wars, and the beginning of countless merchants being drawn into the platform economy.

As an entrepreneur who entered the hospitality industry in 2010, I have been closely involved with food delivery ever since, witnessing firsthand how delivery platforms have shifted from a parasitic relationship with the sector to gradually dominating it. Rogamo has now gone live on delivery platforms too, but the UK food delivery landscape is vastly different from that in China.

This dynamic, comparative perspective made me realise that, after several rounds of delivery subsidy wars, within China’s food delivery sector, platforms, merchants and consumers alike have all forgotten that food delivery was originally just a straightforward service, one that should simply adhere to the principle of ‘who enjoys, who pays’.

◉Rogamo shop.

What is the ‘who enjoys, who pays’ principle?

One afternoon last month, in the central business district of Canary Wharf in London, which should theoretically be peak delivery hours, my friend and I didn’t spot a single delivery rider.

Meanwhile, in the town where I live, the high street is dotted with chain restaurants, including Wagamama and Pho, which have adeptly adapted Asian cuisine for British tastes. On a Sunday two weeks ago, I went there for a bowl of pho. Throughout the two hours I spent dining, the restaurant’s delivery order printer didn’t make a sound, and not a single delivery rider was to be seen on the commercial streets.

◉The high street of the town where the Rogamo shop is located.

In other words, food delivery in the UK has not become as “developed” as it is in China, where traces of delivery services are a constant presence on every street and lane, day and night.

The main food delivery platforms in the UK are these four: Deliveroo, Uber Eats, Just Eat, and Hungry Panda. They are all foreign-owned companies.

Hungry Panda (熊猫外卖 in Chinese) was founded in the UK by a Chinese international student. As our shop’s orders show, the vast majority of users on the platform are Chinese students studying in the UK. Our shop sits directly opposite the flats where many of them live, so it’s common to see delivery riders pop in to collect orders, park their bikes outside, and walk the rest of the way. That said, the students still much prefer having their meals delivered straight to their door.

◉Hungry Panda is a Chinese food delivery platform targeting the overseas Chinese community and international students. The image is a screenshot from a Hungry Panda promotional video. Image source: Hungry Panda official website

Honestly, I’d prefer them to come into the shop. Not only does the food taste better when it’s fresh and piping hot, but more importantly, for the exact same order, the amount that actually lands in our pockets varies drastically between delivery and dine-in. In the UK, delivery platforms charge small food businesses like ours a commission of 35% plus VAT. We only see 58% of the order total return to our accounts.

◉Freshly baked, piping hot flatbreads.

However, I wouldn’t, like many merchants in China, keep delivery prices on par with or even lower than dine-in prices despite already facing high platform commissions. Even when factoring in the need to maintain platform relationships and drive visibility to the restaurant, we still raise delivery prices by 20% to keep our losses down. I’ve had brief chats with a few other successful restaurateurs in town, and their delivery prices are also higher than in-store prices. It’s simply a cost that customers need to bear.

This is precisely the “who enjoys, who pays” principle I’ve been talking about: if you want to save money, come to the shop; if you want the convenience, you must pay for that convenience. It’s only a three- or five-minute walk from the apartment to the shop—just a stone’s throw. But if customers are determined to use this delivery service, they need to cover the necessary costs, paying both the delivery riders and the platform.

For us as shop owners, our costs are fixed. Rent, staff, utilities, and various other overheads do not decrease simply because you’ve ordered delivery. Therefore, in my logic, these additional delivery costs should be borne by the customer.

The Delivery Price War

Last year, as Meituan, JD.com and Taobao Flash Sale engaged in a fierce scramble, I kept a close watch on the situation as a restaurateur. Drawing on my experience in the UK delivery sector, I can offer a comparative perspective.

Over the past six years, I have never witnessed any cut-throat competition between UK delivery platforms, nor any complicated subsidy programmes. As mentioned earlier, UK platforms charge a commission of 35%, which many would consider significantly higher than the rates in China. Yet in China, beyond the headline 20–25% commission, merchants are required to shoulder most of the costs for various subsidies and discount voucher campaigns. Once you factor in all these deductions, the final net income for Chinese merchants ends up being roughly the same as what I take home.

◉A delivery order from the Rogamo shop.

So, the main difference lies in this: the operating model of UK food delivery platforms is straightforward. It is simply a delivery service. I deliver your food, and you pay for the delivery. Commission is deducted from the merchant, and a delivery fee is charged to the customer. The whole arrangement is transparent at a glance, with none of the convoluted tricks or roundabout schemes.

This is how food delivery platforms should normally operate, rather than following the model adopted by platforms in China: they begin with heavy subsidies to lock in all parties, which disrupts the normal cost structures of many merchants, leaving them to go under once those subsidies are withdrawn;

Later, platforms began requiring merchants to co-subsidise customers and attract users, effectively forcing them to give back the subsidies they had initially received. Eventually, platforms stopped subsidising altogether and left merchants to foot the bill alone. Refuse to play along? Customers on the platform would simply migrate to competing restaurants. By the time everyone finally realised the trap, it was already too late. Merchants on these delivery platforms found themselves completely held hostage, stripped of any bargaining power. The only exception was top-tier restaurant brands, where platforms would occasionally leave a little room for negotiation to attract and retain customer flow.

Finally, platforms push you to purchase visibility and buy your way up the search rankings; only then might your shop stand a chance of appearing at the top of delivery listings. Otherwise, by the time customers scroll down to your restaurant, it will be far too late.

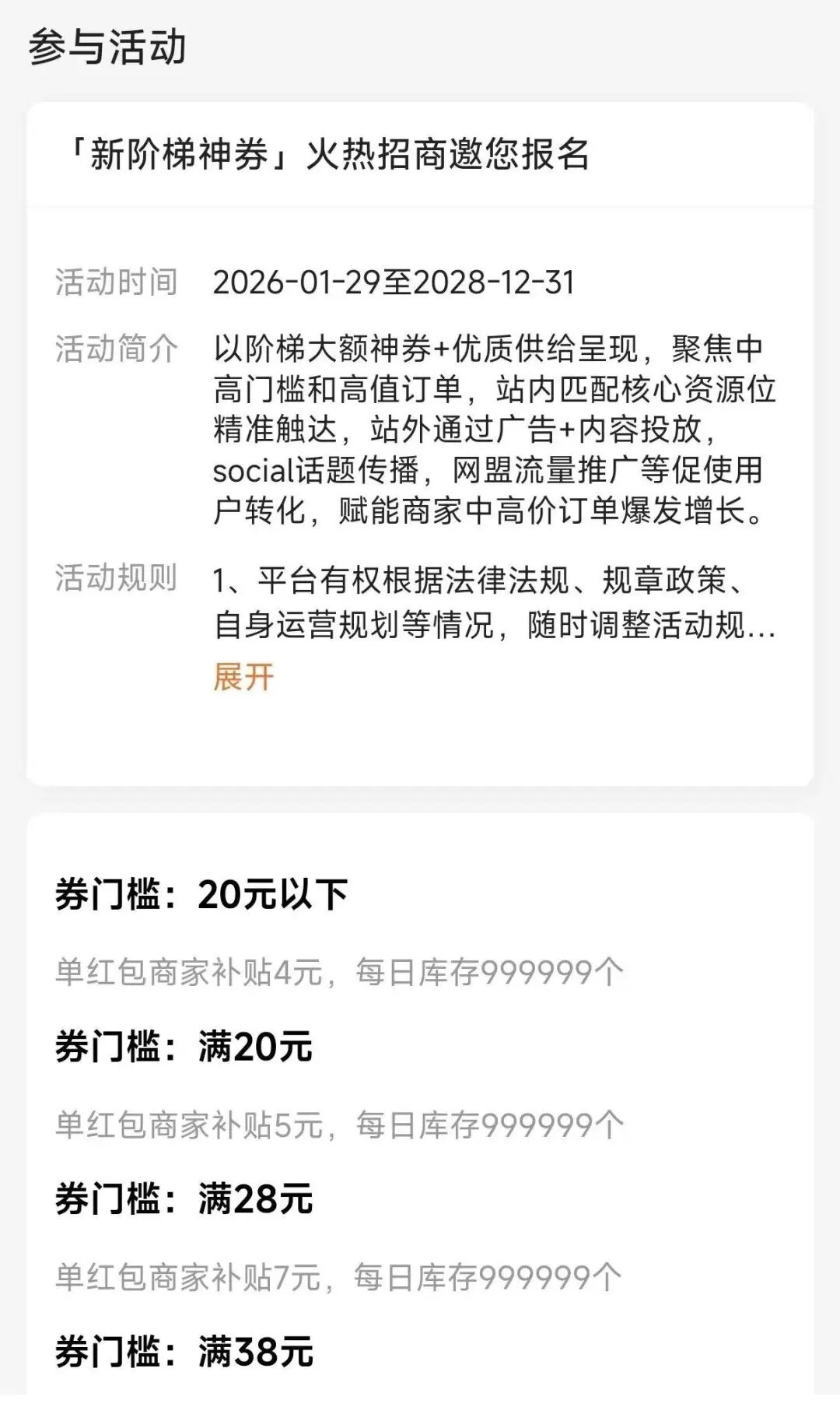

◉This image shows Meituan’s recently launched tiered discount vouchers (阶梯神券) campaign, which has refined the previous five- or six-tier system into nine tiers ranging from ¥0 to ¥128, with the merchant contribution bracket adjusted to ¥5–¥22. Research teams have pointed out that the core of this subsidy adjustment lies not in whether the tiers are more granular, but in how the platform has further shifted subsidy costs onto merchants by adding more tiers. Image source: screenshot from the Meituan app.

Having dealt with platforms continuously since the group-buying era, I have seen things very clearly. During the group-buying war, I told the salespeople who came to my shop for street canvassing: “My shop already has customer flow. Your platforms are the ones trying to acquire users from my store, so you should be paying me.”

When Rogamo first opened six years ago, we went live on all four of the UK’s major delivery platforms. But to this day, whether for dine-in or delivery, I have never done any marketing or promotions, nor offered any discounts. Every time Hungry Panda runs a joint promotion with merchants, they reach out to invite us to participate. I have never joined. I told them: “If the platform is subsidising customers, feel free to do whatever you like. But if it means making merchants pay the subsidies, I will not participate.”

Customers attracted by discounts, subsidies, and promotions are largely unprofitable. They place orders simply to get a bargain, not because your food is good. Drawing on over a decade of experience in the hospitality industry, I know that these customers rarely become regulars once the promotions end; some even leave negative reviews, making the effort not worth it. The customers who truly appreciate your food do so because it tastes good. Our regulars have built up through word of mouth, and to this day, people still occasionally take a two-hour train ride from London just to dine at our shop.

◉There is a young man who visits at least four or five times a week during our six-day operating schedule. Each time, he orders exactly one bowl of braised beef noodles with a side of spicy chili oil. One day, he told me in Chinese, “This is my absolute favourite. No. 1.”

For some more specialised dishes, such as fatty intestine noodles or the occasional old Beijing stewed offal, I do not list them on delivery apps; if you want them, you come to the shop. The main reason is that adding the standard 20% markup would make the online prices even more expensive. When some customers come in for dine-in and see that the same dishes are cheaper than on delivery, they naturally prefer to eat in, which also offers a better experience. In my philosophy of running a restaurant, customer flow should come exactly like this—driven by the food itself, not by platforms or subsidies.

Of course, this logic only holds true because the UK’s delivery platforms have not developed to the point where they can fully control both consumer and merchant resources. This may be related to factors such as the UK lacking the vast pool of cheap labour found in China, a higher degree of consolidation in the foodservice sector, and many chain restaurants operating their own delivery services. Regardless, within this context, we can recognise that the growth of the delivery industry need not be built upon tying merchants’ livelihoods and consumers’ dietary health entirely to a platform’s traffic and profit-driven logic.

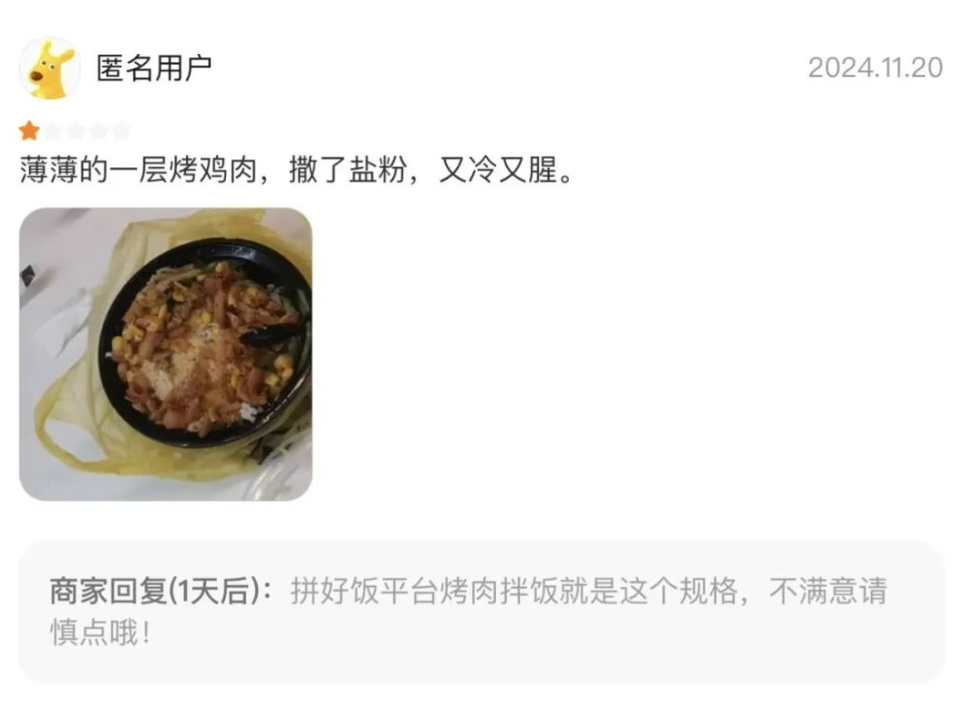

◉Meituan’s Pinhaofan (group-buy meal feature) uses customer traffic as a lever to drive down product prices, forcing merchants to cut costs on ingredients. The image shows user feedback and merchant responses to the service. Foodthink previously described and analysed this low-cost delivery model in “Who Really Gets to Eat Well with Pinhaofan?”. Image source: screenshot from the Meituan app.

It could be said that China’s food delivery industry was essentially born out of abnormal subsidy wars over the past decade or so. After more than ten years, we have almost forgotten what a normal delivery model should look like. Yet as an industry that directly impacts public welfare and health, it is high time we began to seriously consider how the delivery sector ought to develop.

Taking things slowly is actually quite refreshing.

In the UK, ordering food—whether online or in store—and collecting it yourself is a long-standing tradition. Customers would call a restaurant to place an order, and once it was ready, they would simply pop in to collect and pay. The business only needed to focus on cooking and packing the food properly. Even today, now that delivery platforms have penetrated even the British countryside, plenty of takeaways still operate using this phone-ordering system.

Just Eat still offers a vast number of these services, connecting countless takeaways that allow customers to order online but still collect in store. To this day, I believe this is a sound business model for the food industry, given that a restaurant’s practical catchment area is typically just a few kilometres. It allows the business to concentrate on preparing quality food and leave the rest to the customer.

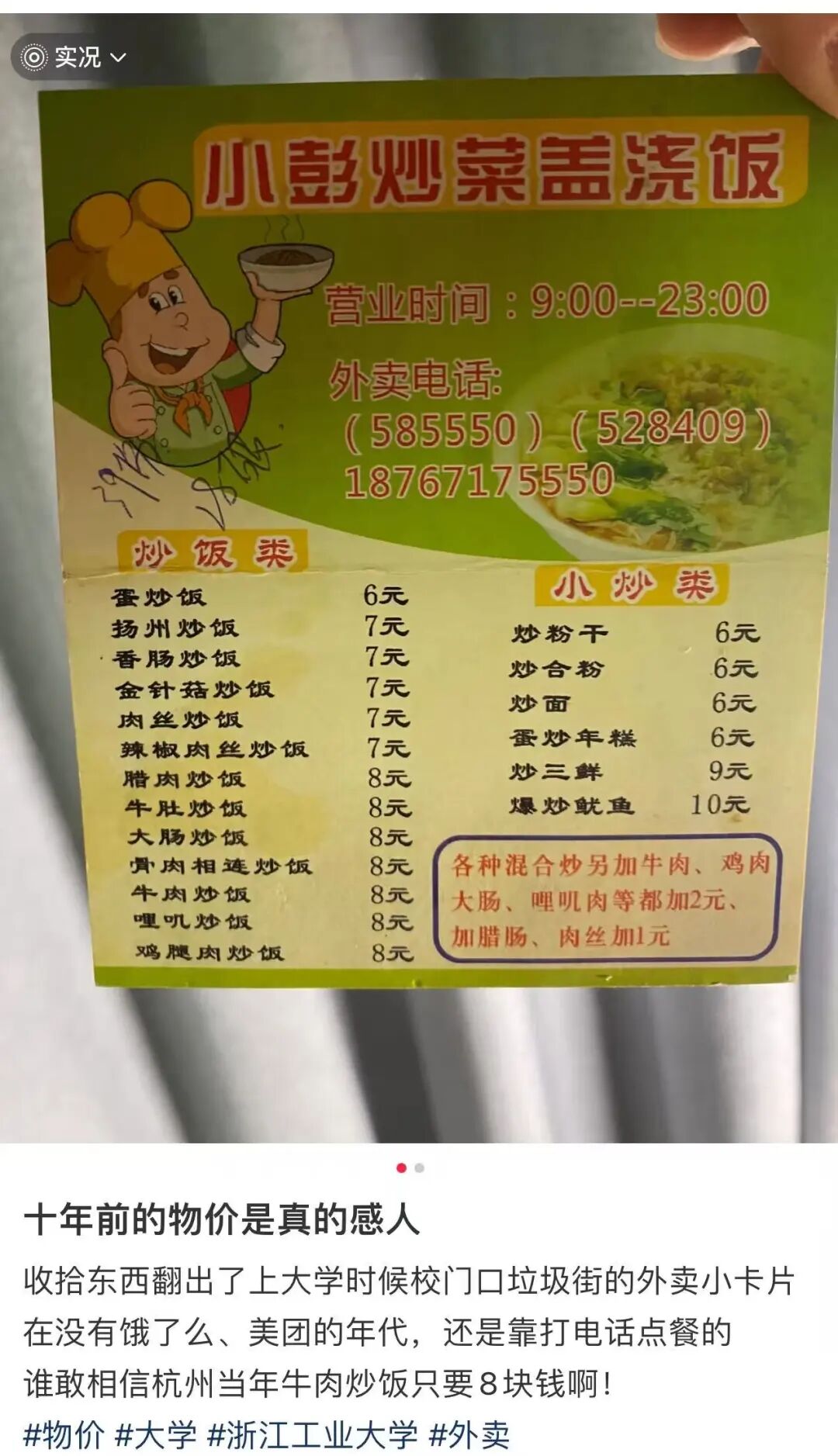

Think back to the five or ten years before delivery platforms arrived: daily life and dining habits in China were nowhere near as frantic as they are today. When I worked at a newspaper office, if we were too busy to go downstairs, we’d order food. Back then, it wasn’t called ‘delivery’; it was simply ‘takeaway’. The system was wonderfully straightforward: local restaurants would leave menus and flyers at the office. We’d call to order, they’d note it down, and once ready, we could either pick it up or have it brought over. The quality back then was identical to dine-in.

◉A user shared a flyer from years ago advertising a restaurant’s own delivery service. Image source: Xiaohongshu @叶不羞的修

Nowadays, the pace of dining and daily life has been pushed ever faster by delivery platforms. Driven by aggressive competition between them, delivery times that once allowed an hour have steadily been compressed to 40 minutes, or even half an hour. The real cost of this speed is riders’ safety and a worrying rise in road accidents.

When it comes to delivery riders, over the five or six years I’ve run my shop in this town, I’ve had hundreds pass through my door, and I know most of them well. I wonder whether UK delivery riders are also bound by strict algorithmic time limits, or have money deducted from their pay for errors. In any case, the riders I see work at a far more relaxed pace; there’s no real rush when they’re making deliveries.

◉A Hungry Panda delivery rider delivering an order. Source: Hungry Panda official website

The people in this town don’t rush their meals, and they’ve gradually grown to love the taste of roujiamo. I’m in no hurry in the kitchen either, quietly putting my own restaurant philosophy into practice here. All in all, taking things slow is just fine.

– This is Foodthink’s 806 th original article –

Foodthink

Author

Ru Tongxue

A restaurant entrepreneur with over a decade of experience, currently writing a book titled *I Sell Roujiamo in the UK*.

Editor: Yu Yang

Layout: Ming Lin

▼

Click the image to read related articles